The U.S. health insurance industry, commonly referred to as Health Maintenance Organization (HMO), is likely to be aided by continued growth in premiums, a solid customer base and consistent contract wins. Despite its solid prospects, the industry has been grappling with escalating costs resulting from continued investments to bolster digital capabilities. Shortage of nurses and inflationary pressure continue to hamper the efficacies of HMO industry players. In spite of the prevailing challenges, companies like UnitedHealth Group Incorporated UNH, Cigna Corporation CI, Humana Inc. HUM and Centene Corporation CNC are better placed to navigate the industry downsides.

About the Industry

The Zacks HMO industry consists of entities (either private or public) that take care of its subscribers’ basic and supplemental health services. Companies in this space primarily assume risks and assign premiums to health and medical insurance policies. Industry participants also provide administrative and managed-care services for self-funded insurance. Services are generally provided by a network of approved care providers (called in-network), which include primary care physicians, clinical facilities, hospitals and specialists. However, out-of-network exceptions are made during emergencies or when it is medically necessary. Health insurance plans can be availed through private purchases, social insurance or social welfare programs.

4 Trends Shaping the Fate of the HMO Industry

Technology Investments Amid a Growing Digital Era: Players in the HMO space are compelled to undertake significant technology investments to stay abreast with the ongoing digital trend. These investments are often directed toward developing telehealth platforms through which the operational efficiencies of healthcare providers receive a boost. Telehealth platforms have exhibited solid demand since the onset of the COVID-19 pandemic as these offered healthcare services within the comfort of one’s home. There are no signs of the demand receding and therefore it seems prudent on the part of HMO players to undertake digital investments. However, bringing its share of worries, these investments might escalate costs and dampen the margins of health insurers.

Nursing Shortage: A notable headwind that has been troubling the U.S. healthcare industry for quite some is an acute shortage of nurses. Health insurers collaborate with several hospitals, as a result of which health plan members of the former can avail hospital treatments at discounted rates. Thereby, health insurers have to depend on nurses and other medical personnel for providing quality managed care services at hospitals per the unique needs of their clients. In the absence of a sufficient nursing workforce, a hospital’s ability to deliver quality services might get affected, which, in turn, may indirectly impact the customer base of a health insurer. A McKinsey report, forecasting that the United States might witness a shortage of 200,000 to 450,000 nurses within 2025, further highlights the dismal scenario that awaits health insurers.

Well-Performing Government Business: The health insurers devise affordable Medicare, Medicaid and Marketplace plans as part of the government business. Frequently, health plans are upgraded with attractive features to retain existing customers as well as attract new ones. Additionally, the HMO players remain on a spree to come up with advanced health plans as that might win them federal or state contracts from time to time. This, in turn, bolsters the customer base and leads to a steady rise in premiums. Increasing premiums bode well for the top line. However, amid the continued inflationary headwind that often takes a toll on the spending habits of consumers, the ability of consumers to continue paying for health plan premiums remain uncertain to some extent.

An Aging U.S. Population: While an aging U.S. population might have been one of the factors contributing to the nationwide nursing scarcity issue, it has definitely been a blessing in disguise for health insurers offering Medicare plans. Meant to benefit people aged 65 or above, Medicare plans are expected to remain in solid demand on account of a growing aging population across the United States. According to Statista, the leading market and consumer data provider, around 16.9% of the American population was aged 65 years or above in 2020 and the percentage is anticipated to reach 22% by 2050. In an effort to bolster the Medicare customer base, the industry participants even operate senior-focused centers for delivering quality care services to the medically vulnerable population.

Zacks Industry Rank Hints Bearish Outlook

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all member stocks, indicates tepid near-term prospects. The Zacks Medical-HMOs industry is housed within the broader Zacks Medical sector. It currently carries a Zacks Industry Rank #217, which places it in the bottom 12% of more than 250 Zacks industries.

Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1. The industry’s positioning in the bottom 50% of the Zacks-ranked industries is a result of the negative earnings outlook for the constituent companies in aggregate.

Despite the dismal scenario, we will present a few stocks that one can buy or retain, given their solid growth endeavors. But before that, it’s worth taking a look at the industry’s recent stock-market performance and the valuation picture.

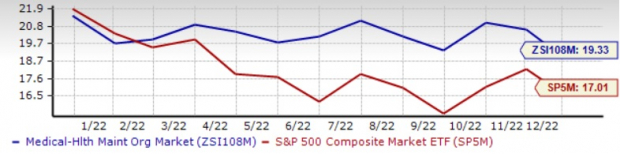

Industry Outperforms S&P 500 & Sector

The Zacks Medical-HMO industry has outperformed the Zacks S&P 500 composite and its sector in the past year.

In the said time frame, the industry has gained 5.5% against the S&P 500’s 20.2% decline and the Zacks Medical sector’s decrease of 20.1%.

One-Year Price Performance

Image Source: Zacks Investment Research

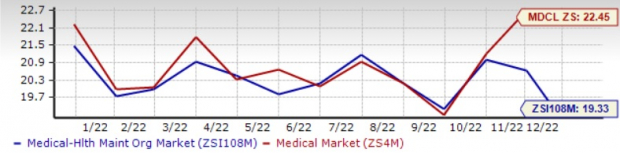

Industry’s Current Valuation

On the basis of the forward 12-month price-to-earnings (P/E) ratio, which is commonly used for valuing medical stocks, the industry trades at 19.33X compared with the S&P 500’s 17.01X and the sector’s 22.45X.

Over the past five years, the industry has traded as high as 21.48X and as low as 19.32X, with the median being at 20.2X.

Forward 12-Month Price/Earnings (P/E) Ratio

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

4 Stocks to Keep a Close Eye on

We are presenting four stocks from the space currently carrying a Zacks Rank #3 (Hold). Considering the current industry scenario, it might be prudent for investors to buy or retain these stocks in their portfolio, as these are well-placed to generate growth in the long haul.

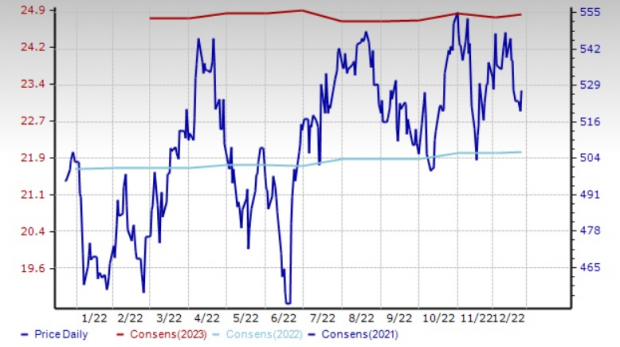

UnitedHealth Group: Based in Minnesota, UnitedHealth Group continues to benefit on the back of strong performances exhibited by its UnitedHealthcare and Optum segments. Several contract wins have resulted in membership growth for UNH. A solid financial position empowers UNH to undertake growth-related investments, which aim to expand its capabilities and solidify its nationwide presence. The healthcare provider has a solid telehealth platform in place that it has developed through continuous partnerships and significant investments. Shares of UnitedHealth Group have gained 6.5% in a year.

The Zacks Consensus Estimate for UNH’s 2022 EPS indicates a 15.8% increase from the year-ago reported figure. The consensus mark for current-year revenues indicates a 12.6% improvement from the year-ago actual. The bottom line of UnitedHealth Group outpaced estimates in each of the last four quarters, the average beat being 4.60%.

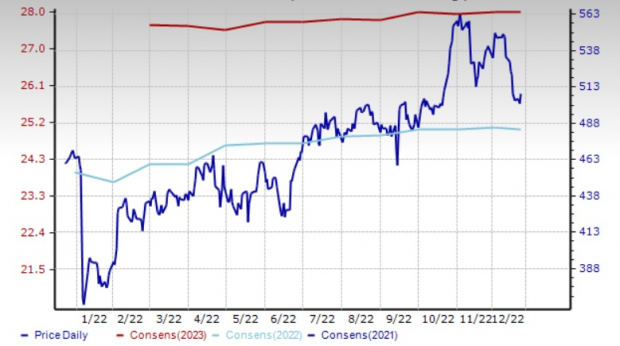

Price & Consensus: UNH

Image Source: Zacks Investment Research

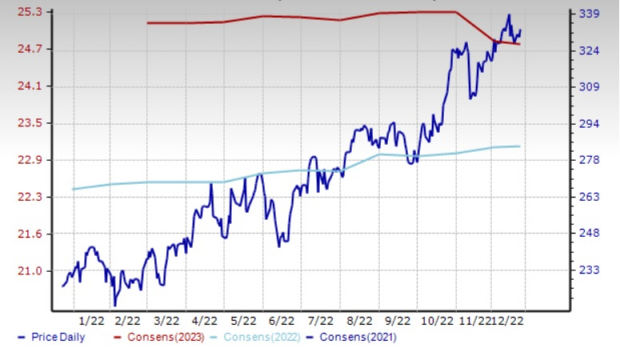

The Zacks Consensus Estimate for Cigna’s 2022 EPS indicates a 13% increase, while the same for revenues suggests 3.2% growth from the corresponding year-ago reported figures. CI’s earnings outpaced estimates in each of the last four quarters, the average surprise being 9.84%.

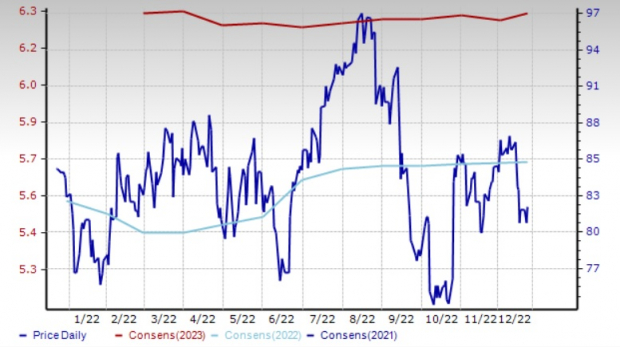

Price & Consensus: CI

Image Source: Zacks Investment Research

Humana: Growing premium revenues arising from an increasing customer base across its Medicaid and Medicare businesses continue to drive revenues of Kentucky-based Humana. The strength of the cost-effective Medicaid and Medicare health plans devised by HUM has fetched numerous contract wins and renewed agreements from Ohio, Louisiana, Oklahoma, South Carolina and Wisconsin for the company. The CenterWell brand, together with Conviva, is part of Humana’s Primary Care Organization, which is one of the largest senior-focused primary care providers in the United States. The stock has rallied 10.3% in a year.

The Zacks Consensus Estimate for HUM’s 2022 EPS indicates a 21.4% increase from the prior-year reported number, while the same for revenues suggests growth of 11.9%. Humana’s earnings outpaced estimates in each of the last four quarters, the average being 10.41%.

Price & Consensus: HUM

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Centene’s 2022 EPS indicates an 11.1% increase from the year-earlier reading. The consensus mark for current-year revenues indicates a 14.7% improvement from the year-ago actual. The bottom line of CNC outpaced earnings estimates in each of the last four quarters, the average being 5.22%.

Price & Consensus: CNC

Image Source: Zacks Investment Research

Zacks Top 10 Stocks for 2023

In addition to the investment ideas discussed above, would you like to know about our 10 top picks for the entirety of 2023? From inception in 2012 through November, the Zacks Top 10 Stocks portfolio has tripled the market, gaining an impressive +884.5% versus the S&P 500’s +287.4%.

Now our Director of Research is combing through 4,000 companies covered by the Zacks Rank to handpick the best 10 tickers to buy and hold. Don’t miss your chance to get in on these stocks when they’re released on January 3.

Be First to New Top 10 Stocks >>

UnitedHealth Group Incorporated (UNH) : Free Stock Analysis Report

Humana Inc. (HUM) : Free Stock Analysis Report

Cigna Corporation (CI) : Free Stock Analysis Report

Centene Corporation (CNC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Source link