Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Newell Brands Inc. (NASDAQ:NWL) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

See our latest analysis for Newell Brands

What Is Newell Brands’s Debt?

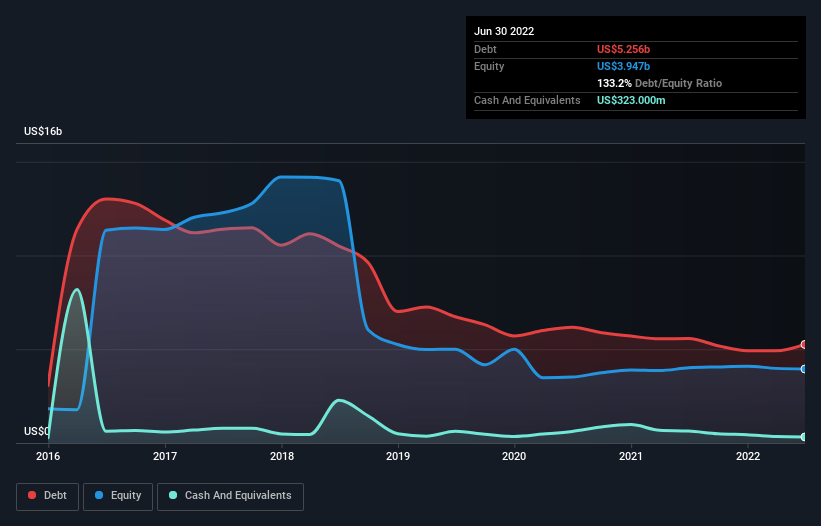

The image below, which you can click on for greater detail, shows that Newell Brands had debt of US$5.26b at the end of June 2022, a reduction from US$5.57b over a year. However, it does have US$323.0m in cash offsetting this, leading to net debt of about US$4.93b.

How Healthy Is Newell Brands’ Balance Sheet?

We can see from the most recent balance sheet that Newell Brands had liabilities of US$4.63b falling due within a year, and liabilities of US$5.87b due beyond that. Offsetting these obligations, it had cash of US$323.0m as well as receivables valued at US$1.56b due within 12 months. So it has liabilities totalling US$8.62b more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company’s US$6.07b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Newell Brands’s debt is 3.5 times its EBITDA, and its EBIT cover its interest expense 4.6 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Unfortunately, Newell Brands saw its EBIT slide 4.7% in the last twelve months. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Newell Brands can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Newell Brands recorded free cash flow worth 71% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

We’d go so far as to say Newell Brands’s level of total liabilities was disappointing. But at least it’s pretty decent at converting EBIT to free cash flow; that’s encouraging. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Newell Brands stock a bit risky. That’s not necessarily a bad thing, but we’d generally feel more comfortable with less leverage. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 4 warning signs we’ve spotted with Newell Brands (including 2 which don’t sit too well with us) .

When all is said and done, sometimes its easier to focus on companies that don’t even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re helping make it simple.

Find out whether Newell Brands is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

Source link